Historically, an Indian investor preferred Fixed Deposits as traditional means of investments. This is largely because of comfort of fixed guarantee of returns in the form of interest with perceived safety of capital. However, with increase in awareness of the need for financial planning, real benefit of risk adjusted returns, ease of liquidity, operational convenience, focus on post tax returns and portfolio diversifications etc debt mutual funds are making foray into retail investors’ portfolio.

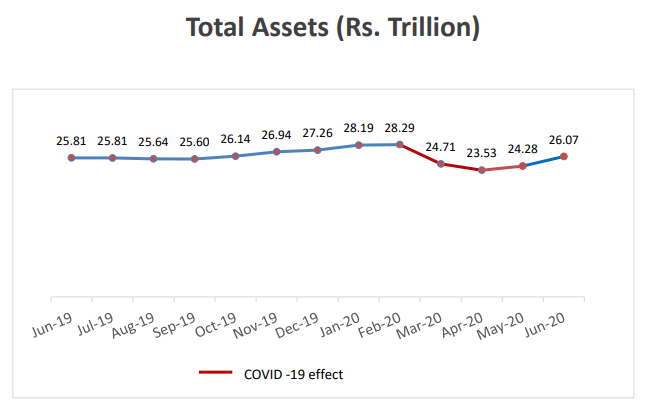

If we look at research study of the last 1 years, it shows that total assets managed by the Indian mutual fund industry has increased from 25.81 trillion in June 2019 to 26.07 trillion in June 2020 amid covid-19 effect.

Source: AMFI Industry trends as on 30th June 2020

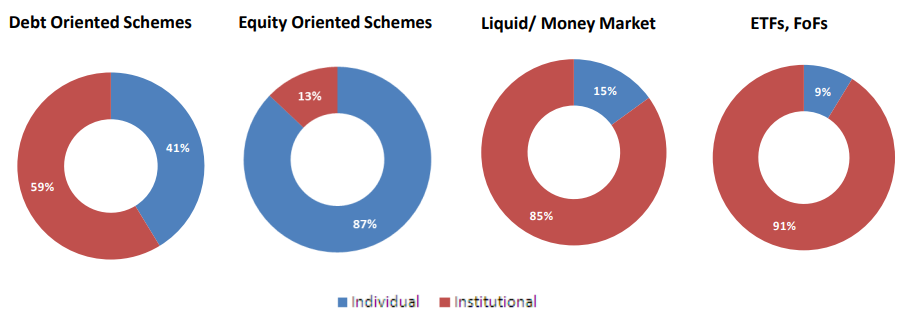

Within Mutual funds Individual investors primarily hold assets under Equity oriented mutual funds with a share of around 87% across other investor categories, debt oriented schmes shares only 41% and Liquid and Money Market shares only 15% – individual investor category across the other category as on 30th June 2020.

Investor category across scheme types

Source: AMFI Industry trends as on 30th June 2020

This shows that the majority of the individual investors are still not aware of the benefits of financial planning through the debt mutual funds over the traditional investments which was time and again continued with the “currency, Time and Fixed Deposits” and ignoring the tax adjusted real returns from debt mutual funds.

Here’s there is real need for you to get aware about the debt Mutual funds to consider debt fund to your asset allocation:

- functioning of debt fund in the market,

- various types of debt mutual funds that suit to your investment horizon and risk profile

- factors that affect the performance of debt mutual funds,

- maximising returns out of money lying idle to your savings account which would be needed after a short period of time,

- using various types of debt mutual fund in journey of achieving your financial goals,

- importance of debt mutual funds in balancing risk in your overall portfolio,

- ease of liquidity in total asset holding in your portfolio,

- fixed and stable income in the form of dividend,

- post tax returns are relatively higher than Fixed Deposits,

- no Income tax deduction at source

Like equity mutual funds, debt mutual funds invest the common corpus (i.e. pool of money) gathered from various investors. The difference is that the equity mutual funds invest corpus funds into shares of the listed companies, debt mutual fund invest in fixed-income or fixed-interest generating opportunities and instruments like bonds, debenture, commercial papers, government securities, certificate of deposits, treasury bills, money market instruments etc bearing fixed interest.

By investing in these fixed income securities, these funds reduces the risk as compared to the equity fund and hence it has low return generating capability in relation to equity funds.

There are various types of debt mutual funds depending upon the maturity duration of the underlying investment instrument. Hence debt funds can be used as a vehicle for investments for Short term, medium term and long-term financial planning at reduced or controlled risk.

Various types of debt funds are summarised for your ready reference to make right decision for investment in debt funds

Types of Debt Mutual Funds

| Purpose of investments | Park Your Savings | For Short Medium- and Long-term investment | Better than Fixed deposit | Others |

|---|---|---|---|---|

| Types of debt Mutual funds and their investment objectives | Overnight Fund For Up to 1 Week | Short Duration Fund For 1 to 3 Years | Banking and PSU Debt fund Invest up to 80% in debt instruments of Banks, PSUs, PFI and Municipal Bonds | Credit risk Funds Invests at least 65% in AA and below rated securities – not so highly credit rated |

| Liquid Fund For 1 week to 1 month | Medium Duration Funds For 2 to 4 Years | Corporate Bond | Gilt Funds Invest 80% in Government securities across maturities |

|

| Ultra-Short Duration fund | Medium to Long Duration Funds For 3 to 5 years | Invest 80% in AA+ and above rated corporate Bonds | Gilt with 10 years constant duration Invest primarily in Government securities with maturities of more than 10 years |

|

| Low Duration Funds For 3 to 9 Months | Long Duration Fund For 5 Years or more | Floater Fund Invests at least 65% in floating interest rate bonds |

||

| Money Market Funds For 6 to 12 Months | Dynamic Bond Funds Investing across duration based on interest rates movements | Fixed Maturity Plan Invest the funds with a fixed period of maturity and having a lock in period until maturity |

||

| Risk- grade | Low | Moderately Low | Moderately Low | Moderate |

Another important thing you should know about the debt funds are various risk factor that affect the performance of the debt funds are:

Interest Rate Risk – A change in interest rates affects the yield of debt mutual funds which in turn affects the return to investors. If the interest rates falls in the overall economy, yield of the debt funds bearing securities with higher coupan rates increases which in turn increases the market price of the debt funds. Hence investor earns relatively higher return during the interest rates fall scenario and vice versa if the interest rates moves up the yield decreases and hence market price of the debt fund may go below the actual purchase price.

Credit Risk – is the default risk of the issuer not repaying the principal and interest. This would lead to a fall in market price of that particular debt fund which does not receive the regular income from its borrower as a result an investor may get a negative return on his investments.

Liquidity Risk – is a risk carried by the fund house of not having adequate liquidity to meet out the redemption requests.

It is always better to park your surplus funds or emergency funds which you know that these funds you are going to spend after a short period of time say 3 to 6 months at low risk in a liquid fund which can at least yield more return than your savings bank account.

When your existing investment in highly volatile equity funds is nearby to achieve your financial goal, you need to be watchful of the corpus so accumulated. You may switch this corpus from a volatile equity fund to the debt mutual funds at low risk well before 1 or 2 years of its actual requirement as further downturn in equity may erode the value of such accumulated corpus, making fall short of your planned financial goal.

The main objective of having a debt fund in the portfolio is that it adds diversification to the asset class and hence low risk-oriented debt fund balances the risk in the overall portfolio. You should also consider your various other factors like age, income source, your current lifestyles spending, and risk level in the existing investments. For instance, higher age group investors must have more proportionate debt fund investment than equity oriented. Similarly having uncertain income flow you must look for the preserving capital investments by investing in low risk category funds i.e debt funds.

Investment in debt mutual funds provide the highest level of liquidity as compared to any other asset class. Since debt funds aims at providing steady and constant growth by way of periodic fixed income it keeps intact your capital fund invested subject to its associated risk factor (as discussed above), Hence you can easily liquidate the investment in case of exigencies

Debt mutual funds can become your fixed and stable income source, be it either at retirement age or during your earning period, if your portfolio sufficiently holds the debt class mutual funds too.

Fixed income under the debt fund is received in the form of dividend which was not taxable in your hands until FY 2019-20. From FY 2020-21 dividend income from debt and equity funds are taxable under normal tax slab along with your normal taxable income.

Capital gain arises on the sale of units of debt mutual funds within 3 years of purchase, short term capital gain if any shall be added to your normal taxable income and taxed as per the applicable tax slab. In case of units sold after holding more than 3 years from the date of purchase shall be taxed as long-term capital gain at the rate of 20% with indexation benefit.

There is no applicability of income tax deduction at source on income/dividend from debt mutual funds scheme.

Thus, in a nutshell you should consider having an appropriate asset allocation strategy of investing in the various types of debt mutual funds that are best suited to you.

You can select one of the top performing fund houses in the debt category and chalk out appropriate asset allocation strategy in various types of debt fund offered by that fund house or you can invest in different types of debt funds across the debt scheme of different fund houses

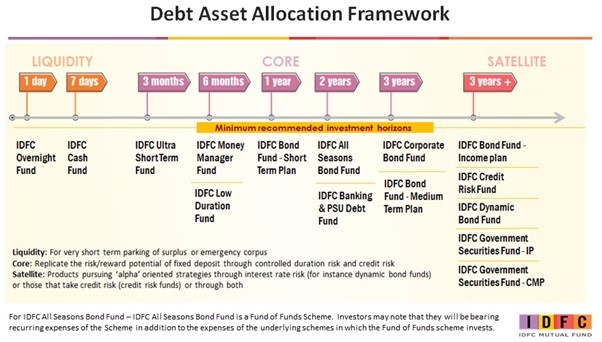

Suggested Debt Asset Allocation Framework with IDFC mutual Fund

There are various strategic ways by which you can use the debt mutual fund as your investment vehicle to create a deep-rooted equity portfolio.

It is always advisable to take help of an expert financial advisor who can chalk up a strategic investment plan for you integrating debt and equity funds in your portfolio that optimum utilization of money among risk, return and safety.

You can contact us at admin@identityinvestments.in or Call us 9920657907 to help you build up a well-integrated diversified portfolio in Debt and Equity funds in a best strategic way.

Below are our few recommended top debt funds schemes across various types you can consider for investments.

| Fund Name | Type | 1Y Returns | 3Y Returns | AUM | |

| IDBI Liquid Fund | Liquid | 5.53% | 6.72% | ₹1264.08 Cr | |

| Kotak Dynamic Bond Fund | Dynamic Bond | 11.24% | 9.63% | ₹1321.52 Cr | |

| DSP Government Securities Fund | Gilt Fund | 12.59% | 9.8% | ₹918.16 Cr | |

| Axis Banking & PSU Debt Fund | Debt | 10.97% | 9.46% | ₹16455.92 Cr | |

| Kotak Corporate Bond Fund | Debt | 10.46% | 8.9% | ₹4607.42 Cr |